The Employee Persona as a Recruitment Strategy

To successfully navigate the current job market, hiring managers should consider what job seekers most value or dislike about a job. That is where employee personas can come in handy.

Not every technology that appeared in the past two decades lived up to its original hype. However, from the moment blockchain was first practically applied in 2008, it was poised to become one of the biggest disruptors of the financial market.

Digital currencies like Bitcoin, Dogecoin, Ether, and others promised a new era of transparent and secure financial transactions with less cost and without intermediaries.

And while cryptocurrencies still haven’t materialized their promise of stability, value, and resilience, blockchain evolved into a force that is transforming businesses and the Internet itself.

Just in 2021, worldwide spending on blockchain solutions reached $6.6 billion. According to research conducted by Gartner, it is expected that the value added by blockchain technology will grow to more than $176 billion by 2025.

A survey conducted by Deloitte in 2021 showed that 45% of all FSI respondents believed that blockchain is vital for the secure exchange of digital information. Still, it’s not only the financial sector going through seismic shifts caused by new technology. Decentralized applications (dApps), smart contracts, and assets are altering the operating models of businesses and government institutions.

Human resources are one of the sectors that will see many benefits from fully incorporating this technology, especially when it comes to talent acquisition and work automation. Almost every process can be improved, from fast, reliable, and inexpensive background checks to more efficient onboarding of new employees.

Blockchain recruitment is set to transform and automate the entire process and make it efficient and unbiased.

It is a game-changing tool that employers can use to find candidates, organize, and distribute job offers more effectively and reliably. This article tries to find out how far away blockchain-based recruitment is, the long-term impacts of the new technology, and the logic behind it all.

Concisely, a blockchain is a data structure that supports the creation of digital information records shared among a network of independent parties. At its core, blockchain is a distributed database that allows secure, transparent, and tamper-proof data storage.

However, unlike a traditional database managed by a central authority, a blockchain is decentralized, meaning that it is spread across a network of computers. This makes it much more difficult for data to be altered or deleted, as it would require the approval of the majority of users on the network.

Blockchain or distributed ledger technology was introduced to the broader public in 2008. A person, or a group, under the alias Satoshi Nakamoto published a paper where they described a new way to store and distribute data with verifiable integrity and decentralized structure. They introduced this technology to support a new type of digital currency, Bitcoin.

Their idea was to eliminate the need for a trusted third party in traditional currency exchanges. They wanted to create an environment where two parties that don’t have a mutual trust can exchange data they can trust without the need for a central authority.

The most significant difference between a blockchain and a conventional database is how the data is stored.

Traditional databases rely on a central location to store data. Clients then connect to the server and can perform CRUD operations (create, read, update, and delete). Even though they are not particularly good at maintaining audit trails of data changes, they are optimized for speed and high throughput.

Unlike a traditional database, blockchain doesn’t support CRUD operations. There is no update or delete options which means that the data is permanently recorded and cannot be changed. Also, its information is stored on every full blockchain node and not one central server, making the entire structure more resilient in case of node failures.

As a digital ledger of transactions, it continuously grows as “completed” blocks are added with a new set of recordings. Each block holds a cryptographic hash of the previous block, a timestamp, and transaction data. They are secure by design.

Today there are many distributed ledger technology protocols in operation (e.g., Bitcoin, Ethereum, Hyperledger, Quorum). Each is slightly different, but they all operate with similar logic.

For example, Bitcoin nodes use the blockchain to distinguish legitimate transactions from attempts to re-spend coins that have already been spent elsewhere. While Bitcoin uses this model only for monetary transactions, it can be utilized in many other ways.

Bitcoin nodes confirm transactions by using a proof-of-work system. All pending ones are bundled into a block, and the algorithm generates a hash number. The resulting number is then compared to a target set by the network. If the hashes match, the block is considered valid and is added to the blockchain. If not, it is rejected and discarded by the network.

Miners receive rewards in bitcoins for their part in the process of verification as an incentive for their work. It helps ensure that the network stays decentralized and healthy.

While there are many diverse types of blockchain, they can broadly be classified into three categories: public, private, and permission blockchains. Each type has its advantages and disadvantages, making it well-suited for different use cases.

For example, public ones are often used for cryptocurrency transactions due to their high degree of security, while businesses often use private ones for internal record-keeping purposes.

Blockchain technology is significant today because of the added security layer it provides in the digital world. Before its first implementation in 2008, trust on the Internet was established by certificates issued by central authorities.

One such example is the SSL certificate (Secure Socket Layer), represented by a closed lock in the browser’s address bar. Unfortunately, SSL certificates have proven not to be foolproof, and hackers were able to steal them from the trusted domains.

With the rise of distributed ledger technology level of trust in the digital space rose to new levels. With its permanent and reliable data storage, businesses got the opportunity to transact online in ways that until recently were possible only offline. Networks establish trust in different ways:

Aside from building trust in the online world, a few additional elements make it particularly interesting technology for all major industries. And while things such as end-to-end encryption or peer-to-peer connectivity are not anything new, blockchain technology allows things to scale quickly.

This means that the companies can quickly verify the sources of their products and oversee the entire supply chain. According to research conducted by PwC Global, just this capability of the technology will improve global GDP by an estimated $960 billion by 2030.

As distributed ledger technology evolves, it will significantly impact many industries. From banking and finance to healthcare and supply chain management, it will offer new opportunities for businesses to streamline operations and drive economic growth. There is considerable interest in the potential application across industries.

Like every emerging technology, blockchain has much hype around its name. It seems that every year people find new ways to implement it. And while some executions haven’t lived up to the initial hype (NFT), there are recent emerging trends that signal its maturing.

One of the most significant downsides is its energy consumption.

Even though cryptocurrencies and miners are using most of that energy, the entire distributed ledger technology got a bad reputation for not preserving the environment.

Bitcoin uses over seven times more energy daily than all of Google’s global operations. POW networks are driving the energy consumption through the roof. Just one single transaction requires the same amount of energy as an average UK household uses in two weeks.

Overall, this volume of energy consumption is unsustainable in a world threatened by climate change and an existing global energy crisis. Which is the reason most blockchain groups look into long-term sustainable solutions.

For this reason, Ethereum decided to switch from POW to POS system completely. Once this transition is completed, Ethereum will drastically reduce energy consumption. The estimate is that merging to the proof-of-stake system could result in a 99.95% reduction in total energy use.

Changes like this, unfortunately, cannot happen overnight. Moving from a legacy system to something new takes much time and effort.

The advantages of blockchain will lead more governments to begin the implementation of this technology in various aspects of their operations. Its immutability and transparency make it ideal for keeping sensitive government data safe from cyberattacks and for identity verification and voting.

Researchers from the University of Coruna, Spain, created an E-Voting System that uses Hyperledger Fabric blockchain and smart contracts.

This decentralized system has the potential to offer a higher level of transparency, security, and cost-efficiency. The casted votes are recorded imminently, providing voters with anonymity and trust in the fairness of the election process. In addition, blockchain-based voting systems can help to ensure the integrity of elections and prevent voter fraud.

The blockchain data structure is an excellent solution for securing sensitive government information from cyberattacks and digitizing operations of almost all government institutions.

A great example of this is Estonia, where 99% of the government services are available to citizens as e-services. Official reports show that Estonia saves over 1400 years of working time and 2% of GDP annually thanks to its digitized public services.

Trust is still one of the most significant issues and obstacles in implementing distributed ledger technology in the public sector on a large scale. World Bank recommends a new “Three Layer” design which consists of:

According to an analysis by one of the world’s top research and advisory firms, Gartner, more than 40% of large businesses will use some HR solution powered by distributed ledger or AI technology by 2022. While AI in HR is nothing new, combining these two technologies opens countless possibilities to improve and automate most HR processes.

Payroll management is probably the most obvious reason to use blockchain in human resources. Still, few other emerging trends will make distributed ledger irreplaceable technology in HR.

Even though most people still associate it with cryptocurrencies, many companies use blockchain for internal purposes. This electronic “ledger” gains more investments from data storing to internal company transactions year after year.

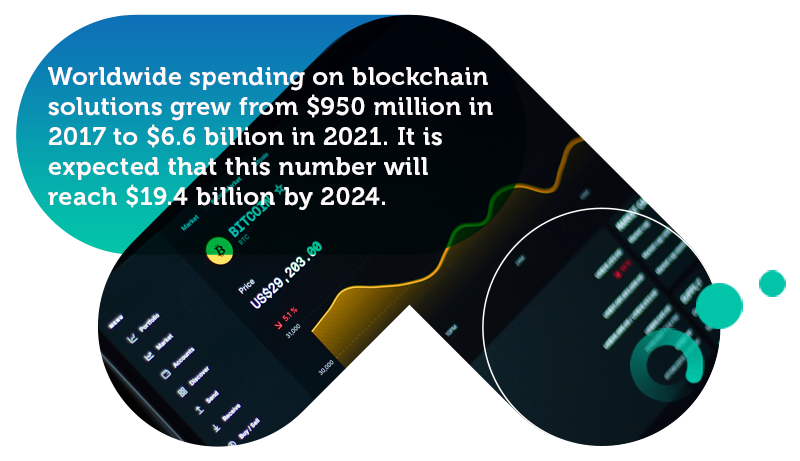

Worldwide spending on blockchain solutions grew from $950 million in 2017 to $6.6 billion in 2021. It is expected that this number will reach $19.4 billion by 2024. In 2020 30% of the global blockchain market revenue was distributed toward the banking sector, 11.4% towards manufacturing, and 4.2% towards the public sector.

According to Vantage Market Research, the global blockchain healthcare market was valued at $287.9 million in 2021, but the value will reach $1.1 billion by 2028.

Increased need to manage a widespread workforce and accelerated digitization and automation of HR operations will drive global HR market value growth to an estimated $30 billion by 2025.

Remote work has become a new reality for most businesses since 2020.

Most companies could operate with their employees outside of their offices, signaling a new era. The ability to work from any place meant freedom for the workers and their employers.

Suddenly, companies had the opportunity to look for new talent worldwide.

Naturally, all this comes with its challenges.

Team members can conduct interviews via Zoom and evaluate the potential candidates remotely. But how do you run a background check on someone across the world? How do you verify their identity or their referrals? The answer is simple, blockchain.

The application of blockchain in recruitment is set to revolutionize how companies find and hire new talent.

By merging this technology with recruiting software, employers will be able to automate most HR processes. So, what are the key advantages of blockchain recruitment?

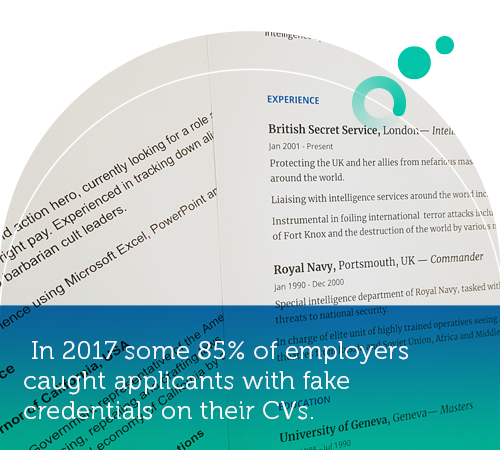

One of the most common problems every recruiter faces is the résumés that are too good to be true. In 2017 some 85% of employers caught applicants with fake credentials on their CVs. This doesn’t surprise since more than a third of people surveyed by HR Drive admitted lying on their résumés.

It is AI tools that are helping recruiters sift through seemingly endless piles of CVs.

But the future is not in spotting the intruders but instead building trust and having a system in place where all candidates will have up-to-date and reliable credentials.

With blockchain technology, a candidate can have all their professional information, employment history, education certificates, social security number, and all other necessary data in one place.

This data can be exchanged with potential employers and instantly verified, providing them with 100% real and accurate resumes.

Having all the necessary data such as electronic signatures, banking information, and social security number instantly available will increase and automate the contracting and onboarding of future employees.

In theory, this means that the person can be immediately hired. In the world slowly shifting toward the gig economy, this will significantly reduce the time and cost of administrative work.

Blockchain technology is still in its pilot stages, but it has already disrupted traditional recruiting models. For example, this technology can create decentralized job boards that allow employers and job seekers to connect directly.

Once the CV is uploaded to a centralized job board in a current setup, the candidate has no control over it. Recruiters can spend days looking through resumes only to discover that the one they have is outdated. With a decentralized system, candidates can instantly update their resumes on every job board when they update their main profile.

A smart contract is a blockchain-based contract that automates the execution and is enforced in real-time. It eliminates the need for the middleman, thus saving organizations time and money. This type of contract is used in various sectors like healthcare, government, real estate, and HR.

Their application in the recruitment process is becoming more critical. In blockchain recruiting, smart contracts can create an immutable record of candidate applications and automatically match candidates to open positions based on skills and experience. They can also automate releasing payments from escrow once the workers complete the task.

Smart contracts can also streamline the onboarding process by automating the creation of employee profiles and the distribution of HR documents. Using them, blockchain-based recruitment platforms can provide a more efficient, transparent, and secure way of connecting employers and job seekers.

The human resources industry in Japan has been going through a dramatic transformation since the beginning of the COVID-19 pandemic. The local job market became increasingly borderless, forcing Japanese companies to explore work styles closer to the global ones. Also, the traditional system where employees were promoted based on seniority was collapsing.

Many employers also allowed their workers to work side jobs, which wasn’t tolerated before in Japan. All this created influx of talent on the market. HR professionals manually checked resumes for skills, work history, and references. Working like this was time-consuming and stretched the capacities of the human resources sectors.

Persol Career Co. and IBM Garage joined forces to tackle this problem. They wanted to develop a better way to verify a candidate’s resume credentials. That system also had to be able to protect the data from hackers and fraudulent activities while offering a simple way for candidates to update information.

IBM Garage experts used the IBM Blockchain Platform to quickly develop a minimum viable product that had the potential to revolutionize resume verification. By using blockchain to store, verify and share employee work history among a network of HR firms, employee organizations, and private companies, they managed to streamline this task.

The human resources industry in Japan has been going through a dramatic transformation since the beginning of the COVID-19 pandemic. The local job market became increasingly borderless, forcing Japanese companies to explore work styles closer to the global ones. Also, the traditional system where employees were promoted based on seniority was collapsing.

Many employers also allowed their workers to work side jobs, which wasn’t tolerated before in Japan. All this created influx of talent on the market. HR professionals manually checked resumes for skills, work history, and references. Working like this was time-consuming and stretched the capacities of the human resources sectors.

Persol Career Co. and IBM Garage joined forces to tackle this problem. They wanted to develop a better way to verify a candidate’s resume credentials. That system also had to be able to protect the data from hackers and fraudulent activities while offering a simple way for candidates to update information.

IBM Garage experts used the IBM Blockchain Platform to quickly develop a minimum viable product that had the potential to revolutionize resume verification. By using blockchain to store, verify and share employee work history among a network of HR firms, employee organizations, and private companies, they managed to streamline this task.

A blockchain is a powerful tool that will automate and streamline many of the processes in HR. Recruitment, payroll, and benefits administration are just a few of the areas that will be affected. It will make these processes more efficient and secure by reducing or ending the need for human involvement in recruitment, onboarding, and payroll tasks.

As this technology continues to develop, we can expect to see even more applications in HR. As with any innovative technology, there will be some growing pains as businesses adapt to the changes brought about by the blockchain, but eventually, it is sure to revolutionize how we work.

Browse our curated list of vendors to find the best solution for your needs.

Subscribe to our newsletter for the latest trends, expert tips, and workplace insights!

To successfully navigate the current job market, hiring managers should consider what job seekers most value or dislike about a job. That is where employee personas can come in handy.

How easy it is to offboard a remote employee? In fact, it might be more complicated. Having an offboarding checklist can help make sure you don’t miss anything.

Unlock essential recruiting statistics for hiring managers, gaining valuable insights to streamline and optimize your recruitment processes.

Since the company’s culture has always been crucial in attracting and retaining talent, HR professionals might struggle with the dilemma: should they hire for culture add vs culture fit?

Used by most of the top employee benefits consultants in the US, Shortlister is where you can find, research and select HR and benefits vendors for your clients.

Shortlister helps you reach your ideal prospects. Claim your free account to control your message and receive employer, consultant and health plan leads.