Identity theft involves stealing personally identifiable information (PII) and using it without permission, usually for deceit or fraud. This data includes anything from date of birth and a social security number to credit cards, medical accounts, and social media accounts.

The identity thief can get this information through a data breach, phishing scams, skimming devices, physical theft of personal belongings, and more.

When the perpetrator uses the stolen PII for illicit financial gains while posing as the victim, that’s called identity fraud.

Although identity theft can happen without identity fraud, these two are almost always correlated and are often used synonymously.

According to the Federal Trade Commission (FTC), in 2022, identity theft was reported 1,107,197 times, with credit card fraud being the main culprit. In fact, in 2022 alone, there were 440,672 reports of this type of threat.

The top-five category also included miscellaneous identity theft in second place with 326,511 reports, followed by bank fraud (156,143), loan or lease fraud (152,583), and employment or tax fraud (103,420).

While the data for 2023 is incomplete, the first three quarters show an improvement compared to the previous year.

However, a new issue has arisen.

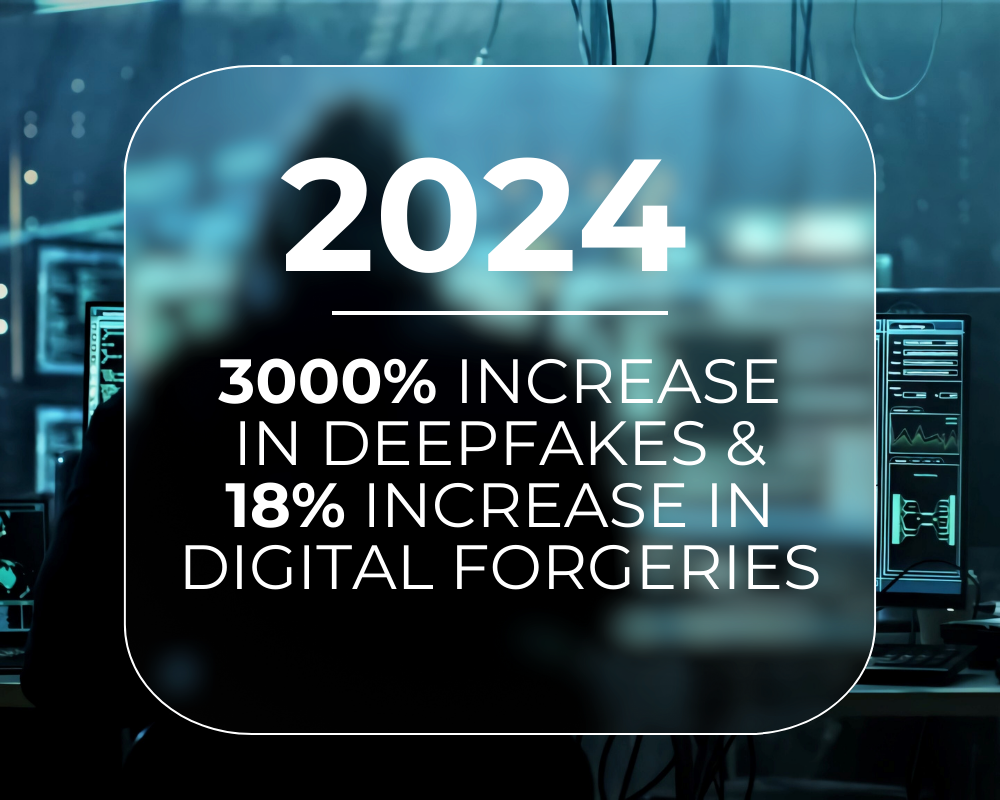

Onfido’s 2024 Identity Theft Report shows a 3000% increase in deepfakes and 18% more digital forgeries. This onset of AI and advanced digitalization opened new opportunities for scammers and fraudsters.

Thus, with such a high incidence of illicit activities, identity theft protection, especially insurance policies, has become a necessity.

But what is identity theft insurance exactly?